Project Overview

This project aims to use machine learning models LightGBM and XGBoost for predicting the target value of insurance premiums, leveraging a dataset with demographic, lifestyle, and policy details to identify key factors influencing premium amounts. The project was a part of a competition hosted on Kaggle in December 2024, aimed for participants to build a prediction model with the lowest Root Mean Square Log Error (RMSLE). There were 2,390 participants with their best RMSLE ranging from 1.01706 (lowest) to 6.68302 (highest). My score is 1.08439.

Python code for the project

The data for this project is available here, on the Kaggle competitions page. Follow the instruction in the dataset description to acquire the data.

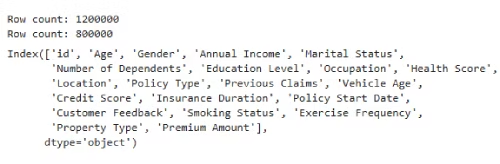

# Importing all the libraries needed import pandas as pd, numpy as np, seaborn as sns, matplotlib.pyplot as plt from sklearn.impute import SimpleImputer from sklearn.preprocessing import OneHotEncoder, StandardScaler from sklearn.compose import ColumnTransformer from sklearn.pipeline import Pipeline from xgboost import XGBRegressor import xgboost as xgb from lightgbm import LGBMRegressor from sklearn.metrics import root_mean_squared_log_error from sklearn.model_selection import train_test_split, GridSearchCV # Set dataframe display options pd.set_option('display.max_rows', 500) pd.set_option('display.max_columns', None) pd.set_option('display.float_format', '{:.2f}'.format) # Import both test and train data train_df = pd.read_csv('train.csv') test_df = pd.read_csv('test.csv') # Check how many rows print(f'Train row count: {train_df.shape[0]}') print(f'Test row count: {test_df.shape[0]}') train_df.columns

# Add a differentiator column for when we merge test and train data train_df['Dataset'] = 'train' test_df['Dataset'] = 'test' # Merge test and train data df = pd.concat([train_df,test_df]) print,(df.shape) df.head(2)

Data Visualization and Analysis

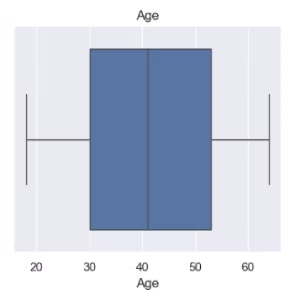

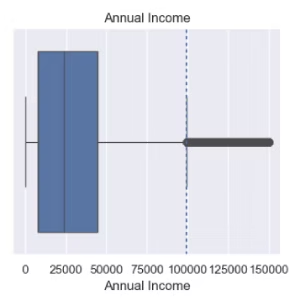

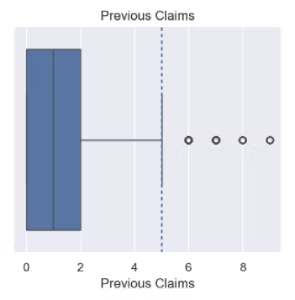

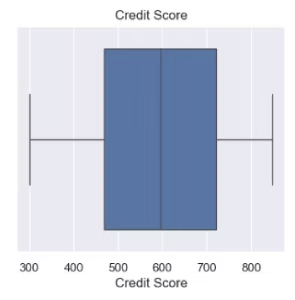

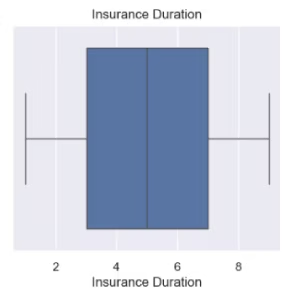

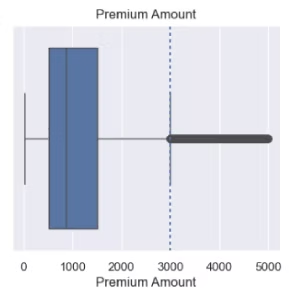

Let’s first visualize the numeric data, and see where (if) there are outliers:

sns.set(rc = {'figure.figsize':(15,15)}) fig, ((ax1, ax2, ax3),(ax4, ax5, ax6),(ax7, ax8, ax9)) = plt.subplots(nrows=3, ncols=3) sns.boxplot(x=df['Age'], ax=ax1).set(title='Age') sns.boxplot(x=df['Annual Income'], ax=ax2).set(title='Annual Income') sns.boxplot(x=df['Number of Dependents'], ax=ax3).set(title='Number of dependents') sns.boxplot(x=df['Health Score'], ax=ax4).set(title='Health Score') sns.boxplot(x=df['Previous Claims'], ax=ax5).set(title='Previous Claims') sns.boxplot(x=df['Vehicle Age'], ax=ax6).set(title='Vehicle Age') sns.boxplot(x=df['Credit Score'], ax=ax7).set(title='Credit Score') sns.boxplot(x=df['Insurance Duration'], ax=ax8).set(title='Insurance Duration') sns.boxplot(x=df.loc[df['Dataset']=='train']['Premium Amount'], ax=ax9).set(title='Premium Amount') incomeQ1, incomeQ3, incomeIQR = df['Annual Income'].quantile(0.25), df['Annual Income'].quantile(0.75), (df['Annual Income'].quantile(0.75) - df['Annual Income'].quantile(0.25)) incomeUpperBound, incomeLowerBound = (incomeQ3+(incomeIQR*1.5)), (incomeQ1-(incomeIQR*1.5)) ax2.axvline(incomeUpperBound, dashes=(2, 2)) claimsQ1, claimsQ3, claimsIQR = df['Previous Claims'].quantile(0.25), df['Previous Claims'].quantile(0.75), (df['Previous Claims'].quantile(0.75) - df['Previous Claims'].quantile(0.25)) claimsUpperBound, claimsLowerBound = (claimsQ3+(claimsIQR*1.5)), (claimsQ1-(incomeIQR*1.5)) ax5.axvline(claimsUpperBound, dashes=(2, 2)) premium_train = df.loc[df['Dataset']=='train']['Premium Amount'] premiumQ1, premiumQ3, premiumIQR = premium_train.quantile(0.25), premium_train.quantile(0.75), (premium_train.quantile(0.75) - premium_train.quantile(0.25)) premiumUpperBound, premiumLowerBound = (premiumQ3+(premiumIQR*1.5)), (premiumQ1-(premiumIQR*1.5)) ax9.axvline(premiumUpperBound, dashes=(2, 2)) plt.subplots_adjust(hspace = 0.5);

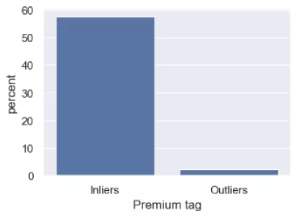

Let’s review the ratio of outlier to inlier data for the three feature having outliers in the boxplots:

df['Premium tag'] = pd.cut(df.loc[df['Dataset']=='train']['Premium Amount'], bins=[0, 3000, 5500], labels=['Inliers', 'Outliers'])

df['Claims tag'] = pd.cut(df.loc[df['Dataset']=='train']['Previous Claims'], bins=[0, 5, 9], labels=['Inliers', 'Outliers'])

df['Income tag'] = pd.cut(df.loc[df['Dataset']=='train']['Annual Income'], bins=[0, 100000, 150000], labels=['Inliers', 'Outliers'])

sns.set(rc = {'figure.figsize':(15,3)})

fig, axs = plt.subplots(ncols=3)

sns.countplot(data=df, x='Premium tag', ax=axs[0], stat="percent")

sns.countplot(data=df, x='Claims tag', ax=axs[1], stat="percent")

sns.countplot(data=df, x='Income tag', ax=axs[2], stat="percent");

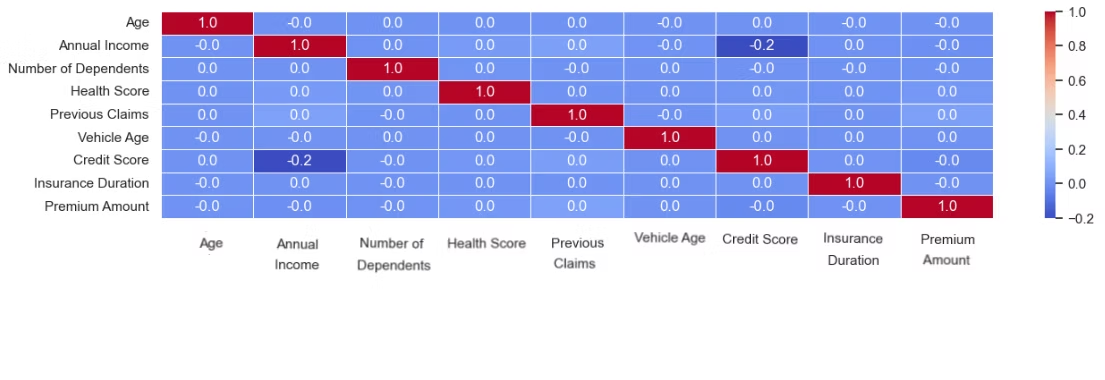

num_data = train_df[['Age','Annual Income','Number of Dependents','Health Score','Previous Claims','Vehicle Age','Credit Score','Insurance Duration','Premium Amount']] sns.heatmap(num_data.corr(), annot=True, cmap='coolwarm', fmt='.1f', linewidths=0.5);

Data Preprocessing

Lets create some new data points and bucket groups

df['Policy Start Date'] = pd.to_datetime(df['Policy Start Date'], format='%Y-%m-%d %H:%M:%S.%f') df['start_year'] = df['Policy Start Date'].dt.year df['start_qtr'] = df['Policy Start Date'].dt.quarter df['start_month'] = df['Policy Start Date'].dt.month df['start_day'] = df['Policy Start Date'].dt.dayofweek df['AgeSegment'] = pd.cut(df['Age'],[17,25,40,55,64], labels=['Young Adults','Adults','Middle Aged','Near Retirement']) df['PremiumSegment'] = pd.cut(df['Premium Amount'], bins=[0, 500, 1000, 1500, 2000, 2500, 3000, 5000], labels=['Very Low', 'Low', 'Around Avg', 'Above Avg', 'High', 'Very High', 'Outlier']) df['IncomeSegment'] = pd.cut(df['Annual Income'],[0,10000,25000,60000,100000,150000], labels=['Very Low Income','Low Income','Mid Income','High Income','Very High Income']) df['HealthScoreSegment'] = pd.cut(df['Health Score'],[1,15,30,45,60], labels=['Very Low','Low','Mid','High']) df['VehicleAgeSegment'] = pd.cut(df['Vehicle Age'],[-0.1,1,5,10,15,19], labels=['New','Fairly Used','Morderately Used','Well Used','Old']) df['CreditScoreSegment'] = pd.cut(df['Credit Score'],[299,580,670,740,800,850], labels=['Poor','Fair','Good','Very good','Exceptional']) df['InsuranceDurationSegment'] = pd.cut(df['Insurance Duration'],[0,3,5,7,9], labels=['New','Loyal','Established','Long-term']) df.head(1)

Make the train test split and encode the categorical and numerical columns/features.

Split the training dataset into the target y data and the features X data. Due to the data columns not having any notable correlations – as seen from Data analysis and Viz, I’ll be using all the columns, except the index columns

X = df[df['Dataset']=='train'].drop(columns=['Premium Amount','id','index','Dataset'])

y = df[df['Dataset']=='train']['Premium Amount']

# Spliting the data using 80/20 split ratio

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

# Further split the X train data by data types so we can encode them properly in our ML pipeline

## For numerical columns, i've used scaling to encode numeric data by their column mean and one hot encoder for the categorical columns

numerical_cols = X_train.select_dtypes(include=["float64", "int64"]).columns

categorical_cols = X_train.select_dtypes(include=["object"]).columns

numerical_transformer = Pipeline(steps=[("imputer", SimpleImputer(strategy="mean")), ("scaler", StandardScaler())])

categorical_transformer = Pipeline(steps=[("imputer", SimpleImputer(strategy="most_frequent")), ("onehot", OneHotEncoder(handle_unknown="ignore"))])

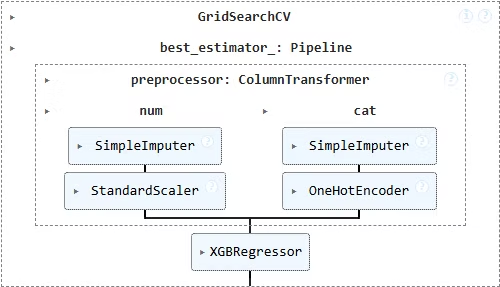

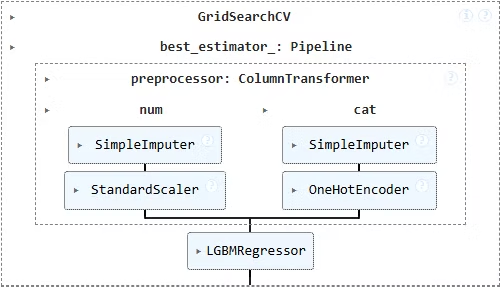

preprocessor = ColumnTransformer(transformers=[("num", numerical_transformer, numerical_cols), ("cat", categorical_transformer, categorical_cols)])

Model Development

# I'll be using the XGBoost and LightGBM models

## LightGBM: Speed and efficiency with large datasets like this one

### XGBoost: Efficient and can be better improved with tuning

lgbm_model = Pipeline(steps=[("preprocessor", preprocessor), ("model", LGBMRegressor(eval_metric='rmsle', verbosity=-1, random_state=42))])

xgb_model = Pipeline(steps=[("preprocessor", preprocessor), ("model", XGBRegressor(eval_metric='rmsle', verbosity=2, random_state=42))])

lgbm_model.fit(X_train, y_train)

y_pred = lgbm_model.predict(X_test)

lgbm_rmsle = root_mean_squared_log_error(y_test, y_pred)

print(f'LightGBM Root Mean Squared Logarithmic Error: {lgbm_rmsle}\n')

xgb_model.fit(X_train, y_train)

y_pred = xgb_model.predict(X_test)

xgb_rmsle = root_mean_squared_log_error(y_test, y_pred)

print(f'XGBoost Root Mean Squared Logarithmic Error: {xgb_rmsle}\n')

- The LightGBM model performed better among the base models

Hyper-tuning

xgb_param_grid = {'model__n_estimators': [50, 100, 200], 'model__learning_rate': [0.01, 0.1, 0.2], 'model__max_depth': [10, 20, None], 'model__objective': ['reg:squaredlogerror']}

xgb_grid = GridSearchCV(estimator = xgb_model, param_grid=xgb_param_grid, scoring='neg_root_mean_squared_log_error')

xgb_grid.fit(X_train, y_train)

lgbm_param_grid = {'model__n_estimators': [100, 200, 500], 'model__max_depth': [5, 10, None], 'model__objective': ['root_mean_squared_error']}

lgbm_grid = GridSearchCV(estimator = lgbm_model, param_grid=lgbm_param_grid, scoring='neg_root_mean_squared_log_error')

lgbm_grid.fit(X_train, y_train)

best_lgbm_model = lgbm_grid.best_estimator_

y_pred_best_lgbm = best_lgbm_model.predict(X_test)

best_lgbm_rmsle = root_mean_squared_log_error(y_test, y_pred_best_lgbm)

print(f"Best Root Mean Squared Logarithmic Error (RMSLE) for LightGBM: {best_lgbm_rmsle},\nBest LightGBM Parameters: {lgbm_grid.best_params_}\n\n")

best_xgb_model = xgb_grid.best_estimator_

y_pred_best_xgb = best_xgb_model.predict(X_test)

best_xgb_rmsle = root_mean_squared_log_error(y_test, y_pred_best_xgb)

print(f"Best Root Mean Squared Logarithmic Error (RMSLE) for XGBoost: {best_xgb_rmsle},\nBest XGBoost Parameters: {xgb_grid.best_params_}")

print(f'LGBM improvement = {best_lgbm_rmsle - lgbm_rmsle}')

print(f'XGBoost improvement = {best_xgb_rmsle - xgb_rmsle}')

Slight improvement for LGBM, but XGBoost tuned up to perform better

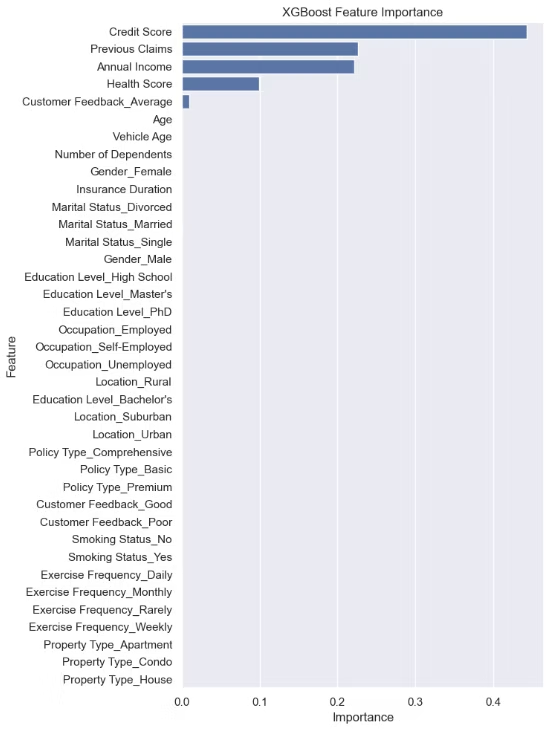

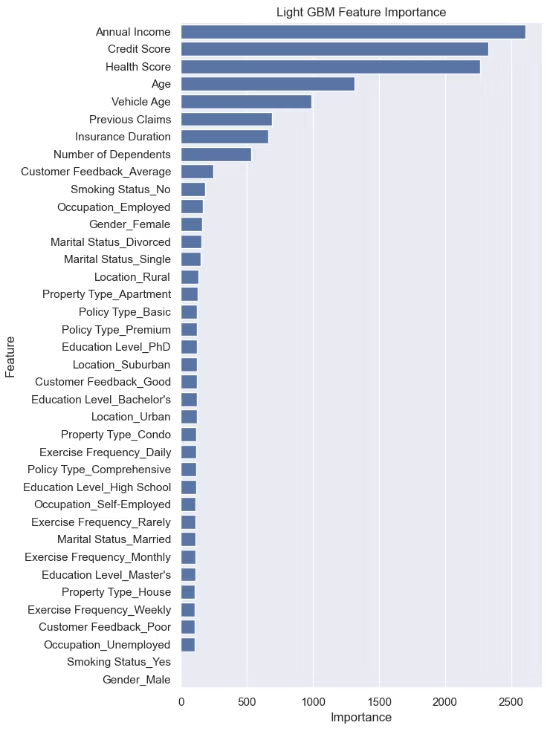

Review key features influencing how premiums are set

lgbm_preprocessor = best_lgbm_model.named_steps["preprocessor"]

lgbm_onehot_encoder_cat = lgbm_preprocessor.transformers_[1][1].named_steps["onehot"]

lgbm_scaler_encoder_num = lgbm_preprocessor.transformers_[0][1].named_steps["scaler"]

lgbm_categorical_features = lgbm_onehot_encoder_cat.get_feature_names_out(categorical_cols)

lgbm_numerical_features = lgbm_scaler_encoder_num.get_feature_names_out(numerical_cols)

lgbm_feature_names = np.concatenate([lgbm_numerical_features, lgbm_categorical_features])

lgbm_feature_importances = best_lgbm_model.named_steps["model"].feature_importances_

lgbm_feature_importance_df = pd.DataFrame({"Feature": lgbm_feature_names, "Importance": lgbm_feature_importances}).sort_values(by="Importance", ascending=False)

xgb_preprocessor = best_xgb_model.named_steps["preprocessor"]

xgb_onehot_encoder_cat = xgb_preprocessor.transformers_[1][1].named_steps["onehot"]

xgb_scaler_encoder_num = xgb_preprocessor.transformers_[0][1].named_steps["scaler"]

xgb_categorical_features = xgb_onehot_encoder_cat.get_feature_names_out(categorical_cols)

xgb_numerical_features = xgb_scaler_encoder_num.get_feature_names_out(numerical_cols)

xgb_feature_names = np.concatenate([xgb_numerical_features, xgb_categorical_features])

xgb_feature_importances = best_xgb_model.named_steps["model"].feature_importances_

xgb_feature_importance_df = pd.DataFrame({"Feature": xgb_feature_names, "Importance": xgb_feature_importances}).sort_values(by="Importance", ascending=False)

sns.set(rc = {'figure.figsize':(15,10)})

fig, axs = plt.subplots(ncols=2)

sns.barplot(data=lgbm_feature_importance_df, y='Feature', x='Importance', ax=axs[1]).set(title='Light GBM Feature Importance')

sns.barplot(data=xgb_feature_importance_df, y='Feature', x='Importance', ax=axs[0]).set(title='XGBoost Feature Importance')

plt.tight_layout();

testing_df = df[df['Dataset']=='test']

testing_df_for_prediction = testing_df.drop(columns=['Premium Amount','id','Dataset'])

xgb_output = best_xgb_model.predict(testing_df_for_prediction)

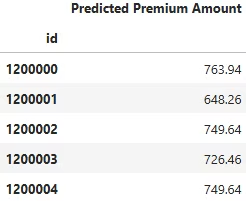

submission = pd.DataFrame({'id': testing_df.index, 'Predicted Premium Amount': xgb_output}).set_index('id')

submission.to_csv("submission_20241230_RMSLE_1.0838731114904818.csv")

# Review top 5 predicted rows

submission.head()

Email: s.o@sesandatalab.com

© 2024 Sesan Data Lab